When it comes to qualifying for a mortgage, your income plays a key role in determining how much you can borrow. For many buyers, especially those interested in investment properties or who plan to rent out part of their home, the question is whether rental income can be counted toward their mortgage qualification. The good news is that in many cases, rental income can help, but there are specific rules and documentation requirements you will need to meet.

When it comes to qualifying for a mortgage, your income plays a key role in determining how much you can borrow. For many buyers, especially those interested in investment properties or who plan to rent out part of their home, the question is whether rental income can be counted toward their mortgage qualification. The good news is that in many cases, rental income can help, but there are specific rules and documentation requirements you will need to meet.

Understanding How Lenders View Rental Income

Lenders want to ensure that any rental income you list is reliable and can be used to make mortgage payments. This means they typically look for documented proof of that income and assess its stability. If you already own a rental property, lenders may use your past tax returns to verify income. If you are buying a new property, they may allow you to use projected rental income if you can provide a signed lease agreement or an appraisal that includes rental value.

Using Existing Rental Income

If you already have rental properties, lenders will generally want to see two years of rental income history on your tax returns. They may use the average income reported over that period, minus expenses, to determine how much can be counted toward your qualification. This helps ensure the income is consistent and not just a short-term boost.

Using Future Rental Income

If you are buying a property that you plan to rent out, such as a duplex, triplex, or a single-family home with a basement apartment, lenders may allow you to use a portion of the projected rent toward your qualification. This often requires a market rent analysis or a signed lease, and lenders will typically only count a percentage of that income, usually around 75 percent, to account for potential vacancies and expenses.

Owner-Occupied vs. Investment Properties

The rules for counting rental income may differ depending on whether you are buying a primary residence with a rental unit or a dedicated investment property. For owner-occupied properties, lenders are sometimes more flexible with projected rental income. For investment properties, they often require more documentation and may have stricter qualification standards, including higher down payments.

The Impact on Your Debt-to-Income Ratio

Rental income can help lower your debt-to-income ratio, making it easier to qualify for a larger mortgage. Since lenders compare your monthly debt payments to your gross monthly income, adding rental income to the equation can make your financial profile more favorable. However, it is important to remember that lenders may not count 100 percent of the rent, so plan accordingly.

Documentation Is Key

To use rental income for mortgage qualification, be prepared to provide the necessary paperwork. This could include signed lease agreements, tax returns with Schedule E, property management records, or an appraisal with a rental analysis. The more organized and complete your documentation, the smoother the process will be.

Yes, you can often use rental income to qualify for a mortgage, but it depends on the type of property, your history as a landlord, and the documentation you can provide. Working with a knowledgeable mortgage professional can help you navigate the rules and make the most of your rental income when applying for a loan.

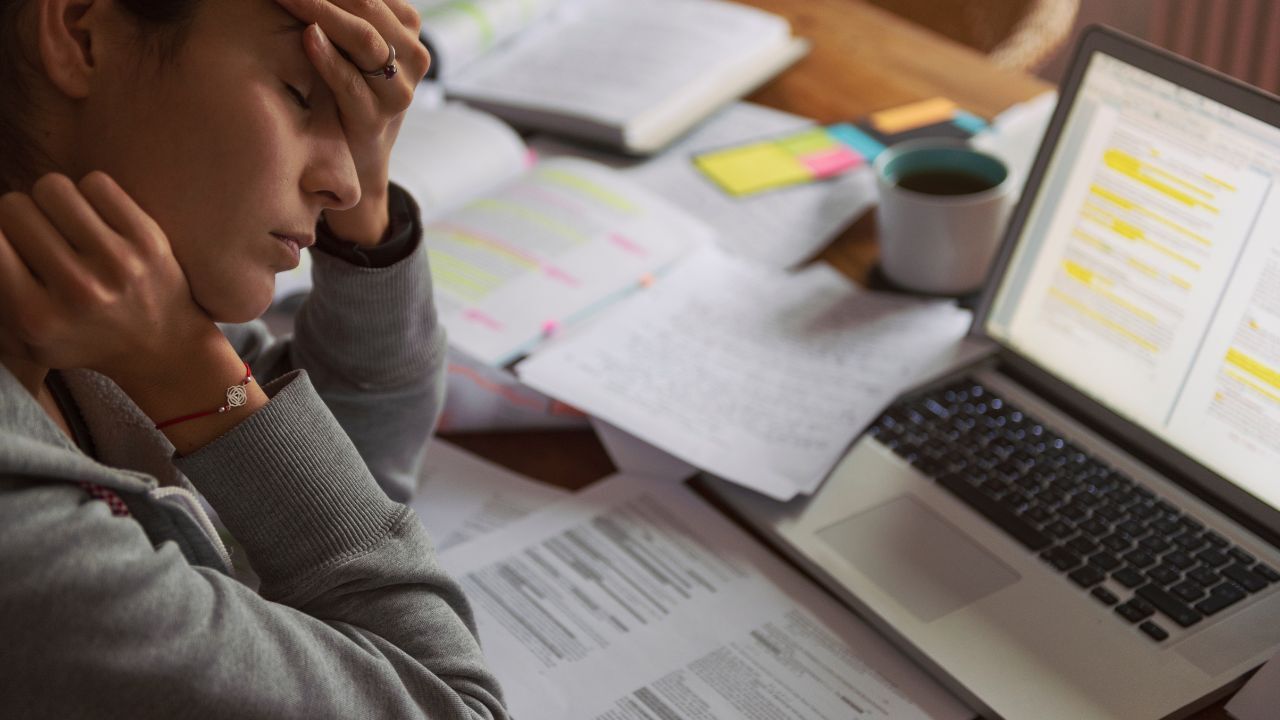

Buying a home is one of the most exciting milestones in life, but it can also be one of the most exhausting. From house hunting and comparing loan options to managing the financial paperwork and deadlines, the process can become overwhelming. Mortgage burnout happens when the stress and demands of the home buying journey begin to wear you down, making it harder to stay focused and positive. The good news is there are ways to protect yourself from burnout and keep the process manageable.

Buying a home is one of the most exciting milestones in life, but it can also be one of the most exhausting. From house hunting and comparing loan options to managing the financial paperwork and deadlines, the process can become overwhelming. Mortgage burnout happens when the stress and demands of the home buying journey begin to wear you down, making it harder to stay focused and positive. The good news is there are ways to protect yourself from burnout and keep the process manageable. Many potential homebuyers worry that carrying credit card debt will prevent them from qualifying for a mortgage. While it is true that lenders carefully evaluate your financial profile, having credit card balances does not automatically disqualify you. By understanding how lenders view debt, taking strategic steps to improve your application, and choosing the right mortgage program, you can still achieve your goal of homeownership.

Many potential homebuyers worry that carrying credit card debt will prevent them from qualifying for a mortgage. While it is true that lenders carefully evaluate your financial profile, having credit card balances does not automatically disqualify you. By understanding how lenders view debt, taking strategic steps to improve your application, and choosing the right mortgage program, you can still achieve your goal of homeownership.